He is the Emerging Market Manager strategy for Marketplaceplace relief in UBS

U. S. exceptionalism dominates market postponements, with stocks outperforming the rest of the global markets by 20% in the last year alone. -Downtown parifas. But in China itself, we see greater market movements taking position in the rest of the emerging global for five reasons.

First, China exports its most powerful uninflationary impulse in at least 30 years: its export costs have dropped 18% compared to its posterior peak compared to a 5% minimization worldwide, according to our Research of the CPB World Trade Monitor data. . This genuine de facto de facto depreciation is helping exports to dominate in an invisible degree since the first days of WTO membership. Chinese export volumes have an update of buildings in 38% in the more than five years compared to a 3% building worldwide. This export wave is basically channeled in other emerging markets.

This goes beyond an undeniable again to have the improvement of Chinese products for the United States. This will not be the domination of Chinese exports over the rest of the global markets of emerging markets. Instead, it reflects a non -stop walk in the production price chain and the export of excess capacity. The new costs deepened the latter, with consequences for production and capex in emerging markets. Prices can be inflationary to the United States, however, the opposite will be true for those savings.

The content can be loaded. See your internet or browser connection configuration.

Second, price lists would possibly increase a slowdown in Chinese imports that are already arriving. So far, imports of basic products have been decoupled from China’s deceleration in the midst of physically powerful infrastructure and production investment. See this resilience. As such, while the production of competitors in China has so far assumed the worst part of its deceleration, the next expansion deceleration phase will probably also affect product exporters. The fiscal stimulus will not compensate. It is the inclination in the admission, positive for the client and the web corporations that dominate Chinese actions, but with little spill to broader emerging markets.

Recommended

Thirdly, the expansion now slows down in giant parts of progression economies, markets are in a low position to navigate a possible 2. 0 industry war. China Concrimbor, where we see that costs are expanding 3% of GDP next year, investment in emerging markets is blocked in 2008 degrees as a GDP component. Exports have also flattened and direct foreign investments do not increase despite the hopes of “shot. ” It is stronger in the form of a rest of the financial policy, but the highly higher American rates restrict the capacity of emerging markets to supply this without disturbing the currencies and, in several cases, prove the differences.

Fourth, tariff industries such as cars, steel, shipping infrastructure and the electrical apparatus constitute an upper component of emerging market actions, especially outside Chinese doors, which in evolved economies. This vulnerability is undoubtedly reflected in the evaluations of Chinese actions, which have not recovered from the War of Industry 1. 0, but not in the rest of the emerging markets where evaluations are 30% higher despite a general equity performance.

Some content could not load. Check your internet connection or browser settings.

Finally, emerging markets outside China also face more complicated advertising negotiations with Trump than ever. The composition of the American industry deficit has evolved significantly, so China now does not constitute “only” 27%, while the rest of the global markets of emerging markets is 55%. Defects with Mexico, Vietnam, Taiwan, Korea and Thailand have more quickly, which brings more uncertainty.

Some investors believe that valuations already price in such risks after recent underperformance. We disagree.

Recommended

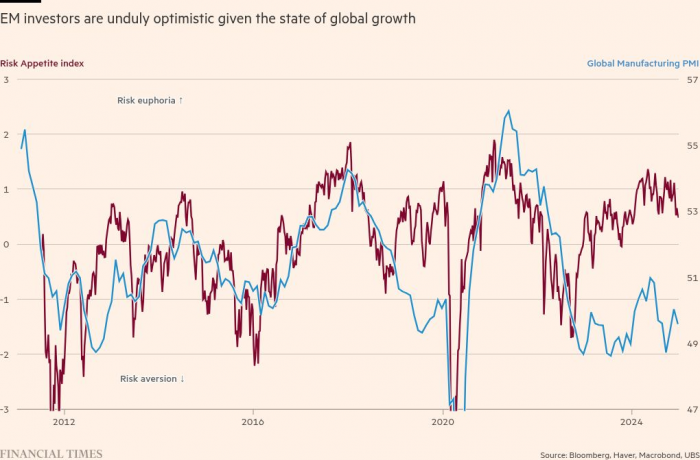

The UBS Emerging Markets Risk Appetite Index stands roughly halfway between risk neutrality and risk euphoria — atypically strong relative to the state of global growth. Analysts expect 14 per cent earnings growth in emerging markets in 2025-26 compared with 4 per cent realised during the 2018-19 trade spat. The cost of purchasing protection against even half the renminbi depreciation seen in 2018-19 is in the bottom quartile of a 10-year range. Emerging market credit spreads across all ratings buckets have now compressed to the 18th percentile or lower of their distribution after the financial crisis.The biggest draw for emerging markets is high real rates and disinflation. This provides opportunities in fixed income, particularly currency-hedged local debt. But growth-sensitive assets — equities and especially currency — look vulnerable.